文

A

Over the past few years, simulation-management games have once again become a frequently discussed direction in China's domestic game market.

Data shows that in 2025, China's mobile casual game market generated RMB 34.265 billion in revenue, up 9.56% YoY. Although the simulation-management segment has not been separately disclosed, from the product side, simulation-management titles have maintained an average annual growth rate of over 25% for three consecutive years, making them a core growth engine in the casual game market.

Compared with categories such as SLG, MMO, and anime-style card games, which rely more heavily on high-intensity stats, competition, and content consumption, simulation-management games naturally follow a different user logic. They do not necessarily require players to stay online for long periods or rely on complex controls. Instead, through planting, production, construction, decoration, collection, and character companionship, they keep players returning to a relatively stable virtual space during fragmented time. This product logic aligns well with players'demand for a slower pace in recent years, bringing themes such as farms, restaurants, courtyards, towns, and homes back into the spotlight.

At present, based on their development sequence, simulation-management gamescan generally be divided into five main directions: traditional farm/town management, heavy-stat business management, light Chinese-style management (the underlying gameplay of the above three directions is more similar, with more traditional monetization), life simulation (mainly monetized through decoration and cosmetics), and mini-game-integrated light management (hybrid monetization).

However, a hotter market does not mean products are easier to succeed. Simulation-management games usually have a low entry barrier, but the real challenge lies in long-term operation. Light management games can easily fall into homogenization; life simulation requires even more content volume, social design, and live-ops cadence, and if monetization becomes slightly too heavy, it will undermine players' expectations for relaxation. If content updates are too slow, veteran players can easily slip into a low-engagement maintenance mode. In other words, thiscategory may look gentle on the surface, but it actually tests a team's long-term control over cadence, content, and user emotions.

Yet as the market continues to wash out weaker products, evergreen titles always remain.

Developed by Area 51 Studio and published by Tencent Aurora Studio, Taoyuan: A Place Deep in the Mountains is one of the representative products in the light Chinese-style management direction. Its China server has been operating for more than three years, and on June 18, the game launched in Japan under the title Rourou no Sato: A Mysterious Life in a Miniature Garden.

01

Taoyuan continues to perform steadily in China, generating US$4.8 million on iOS in 2026

The Japan server begins open beta, aiming to find new incremental growth

The gameplay of Taoyuan: A Place Deep in the Mountains is not complicated. At its core, it follows a typical light simulation-management loop: planting crops, collecting materials, processing them through workshops, and then using the output to complete orders, construct buildings, unlock areas, and advance the story. Its focus is not on making the production chain overly complex, but on ensuring every step serves the feeling of managing a pastoral retreat. After logging in, players have clear tasks to do without strong pressure; orders, buildings, and land clearing provide growth goals, while home decoration turns numerical progress into visible spatial changes.

Compared with management games that focus solely on efficiency, Taoyuan's advantage lies in tightly combining a low-barrier loop with emotional experience. Little radishes, villager stories, Chinese-style scenery, and courtyard decoration together reduce the mechanical feeling of harvesting crops, making it easier for players to see the space as their own life environment. The game does not rely on intense competition or high-frequency daily tasks to maintain retention. Its core appeal comes from stable return visits, slow-paced progression, and sustainable spatial decoration. This also makes it more suitable for long-term operation: new content can expand around buildings, stories, seasonal events, and decorations without forcibly increasing numerical pressure.

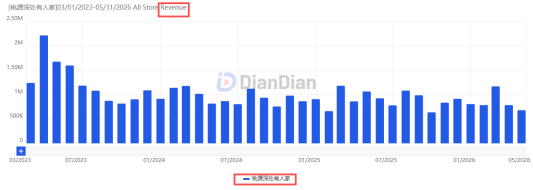

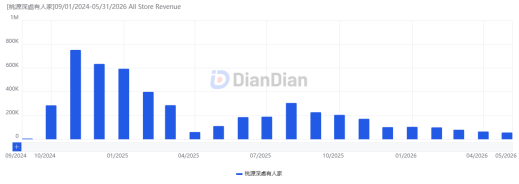

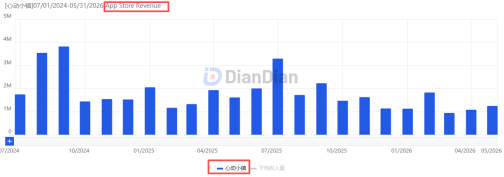

On March 22, 2023, Taoyuan: A Place Deep in the Mountains entered open beta in mainland China and generated US$2.62 million in iOS revenue in its first month (approximately RMB 17.72 million). Although the data declined afterward, it quickly stabilized. Since the second half of 2023, its monthly iOS revenue has fluctuated between US$700,000 and US$1.2 million (approximately RMB 4.5 million to RMB 8 million).

In October 2024, the game launched in Hong Kong, China / Macao, China / Taiwan, China, with first-month revenue estimated at around US$850,000 (approximately RMB 5.6 million). Its data then declined steadily, and current monthly revenue is only US$57,000 (approximately RMB 400,000).

After encountering setbacks in Hong Kong, China / Macao, China / Taiwan, China, Taoyuan: A Place Deep in the Mountains chose Japan as its next new incremental market, given Japanese users' high acceptance of fresh pastoral Chinese-style aesthetics and slow-life simulation-management gameplay.

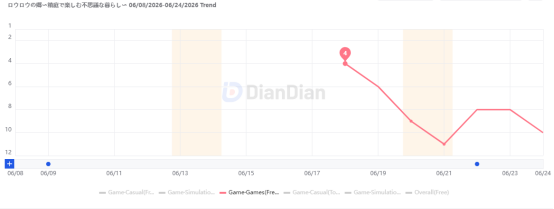

According to DianDian, after the game launched in Japan, on its first day (June 18)it climbed to No. 4 on the iOS free games chart. It then began to decline slowly and currently ranks No. 10 on the free games chart, while it has not entered the iOS games grossing chart.

In terms of downloads, the title opened pre-download one day earlier and recorded 33,000 daily downloads that day. Downloads fell to 21,000 on the first day of open beta and then to 15,000 on the second day.

In terms of revenue, the game generated around US$2,700 on the first day of open beta (approximately RMB 18,000), and rose to US$4,850 on the second day (approximately RMB 33,000).

Across the first two days of the Japan open beta, the game accumulated around 69,000 downloads and an estimated total revenue of US$7,700 (approximately RMB 52,000). The data itself is not especially outstanding. This is directly related first to relatively low user acquisition, second to the audience fit of Chinese-style themes, and third to the fact that the simulation-management market has already shifted significantly toward life simulation.

Image source: GuangDaDa

Finally, although the Japan server's current performance is not strong, the observation window is still too short, and changes may still occur later. As a classic title that has been validated over the long term in the domestic market, Taoyuan: A Place Deep in the Mountains does have the foundation and possibility to find a second spring.

02

Dream Home shuts down quietly, while Heartopia thrives during the same period

Beyond its own issues, the shift in the simulation-management genre is crucial

Also in mid-June, another product within the broader simulation-management category formed a stark contrast with Taoyuan: A Place Deep in the Mountains as it tried to open up new markets: POP MART's self-developed designer-toy-themed “simulation management + party mobile game,” Dream Home.

On June 12, the game issued a shutdown announcement, stating that top-ups, new user registration, and downloads across all platforms would be closed that same day, with official termination of service scheduled for August 12.

Public information shows that Dream Home began development as early as 2018, bringing together popular IPs such as Molly, Dimoo, SKULLPANDA, and LABUBU. It was POP MART's first attempt at turning its IP into a game. The game received its license in 2019 but did not enter open beta until June 27, 2024.

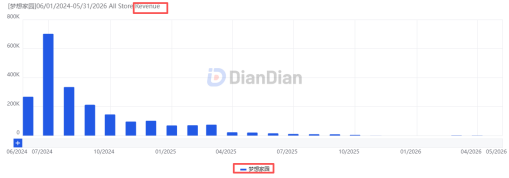

In its first month of open beta, the game generated around US$905,000 in iOS revenue (approximately RMB 6.12 million). While this was not an exceptionally strong result, it was still clearly above the passing line. However, overall performance then fell sharply. By October 2024, monthly iOS revenue had already dropped below US$150,000 (approximately RMB 1 million), and current monthly iOS revenue is even below US$2,000. Since launch, its cumulative iOS revenue has reached US$2.18 million (approximately RMB 14.71 million).

Monthly iOS revenue trend of Dream Home since open beta

As for why Dream Home reached its endpoint only two years after launch, POP MART provided some analysis at last year's annual shareholders' meeting.

First, the game's internal score at launch was only 80, making it difficult to compete against a group of 100-point or even higher-scoring products in the simulation-management market. Second, the team lacked experience in game promotion and operation. Regarding the former, the game did not sufficiently reach the overlapping audience between the IP and the game. Regarding the latter, player feedback showed that the game lacked long-term content updates, had thin gameplay, insufficient technical optimization, and a slow update cadence, leading to a continuous decline in user retention. Finally, the broader simulation-management market was highly competitive.

In fact, 2024, the year Dream Home launched, was indeed the moment when the simulation-management category began shifting toward the life simulation subsegment and showed early signs of breakout growth.

On July 17, 2024, less than a month after Dream Home, XD's life simulation game Heartopia entered open beta in mainland China. The game does not focus on managing assets, but instead emphasizes a “slow pace + freedom without restrictions,” aiming to provide players with a healing and leisurely experience. There are no stamina limits or daily tasks in the game, and players can freely choose activities such as decoration and construction, fishing, cooking, and cat raising.

In its first month of open beta, the China iOS version generated US$4 million (approximately RMB 26.74 million), far ahead of competitors. This level of performance was maintained until September of the same year. Although monthly revenue later declined, it has remained above US$1 million, and current monthly revenue is around US$1.25 million (approximately RMB 8.5 million).

Monthly iOS revenue trend of Heartopia China server since open beta

As of now, after two years of open beta, the game's estimated cumulative iOS revenue in mainland China is US$42.1 million (approximately RMB 285 million), making it the best-performing life simulation product in China.

It is also worth noting that Heartopia's overseas performance has been very strong.

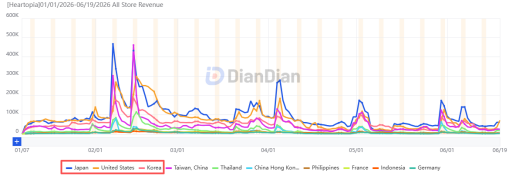

On January 8 this year, the international version Heartopia officially launched in more than 170 countries and regions overseas, generating US$10.5 million in its first month (approximately RMB 70.8 million). Although the data declined afterward, the drop was not significant, and current monthly revenue is around US$8.3 million (approximately RMB 56 million).

Revenue trend of Heartopia since its official global launch

As of now, six months after the international version launched, its cumulative revenue is estimated at US$63 million (approximately RMB 424 million), with Japan, the U.S., and South Korea ranking as the top three markets at 24.82%, 20.9%, and 14.09%, respectively.

03

Life simulation has become a “must-fight” battleground for major publishers

To secure a breakout hit, products must deliver rich content, low pressure, and restrained monetization

Overall, although long-running products such as Taoyuan: A Place Deep in the Mountains, which are lightly optimized within a traditional simulation-management framework, still have market space, life simulation is clearly set to carry greater weight in the future over the longer term, and may even siphon off the profit space of the former.

However, the contradictions within life simulation are also very pronounced: development cycles are long and content costs are high, yet it is difficult to build a stable payment model based on numerical strength as SLG and card games do. Players expect healing, companionship, and immersion, but once monetization becomes too heavy, that experience is damaged. If products rely only on restrained spending such as cosmetics and furniture, it is difficult to support high development and user-acquisition costs. Meanwhile, life simulation requires extremely rich content. If the world is not solid enough, it can easily become a shallow “slice of life.” Products that truly break through must have their own experiential focus, rather than merely copying the shell of an “ideal life.”

Clearly, mid-tier publishers will find it difficult to master this category.

Looking at the product side, although Heartopia still firmly occupies the leading position in life simulation, it is far from monopolizing the category. Since last year, major publishers have clearly begun to make moves, and this year activity has become even more frequent, suggesting signs of a major battle ahead.

At the beginning of the year, Project Lovania, a life simulation game self-developed by LightHouse Studio under MOONTON, began its first test. Its distinctive fantasy picture-book art style and highly free open-world gameplay brought players a strong sense of freshness;

In mid-March, Silver Heart Studio under Tencent's Northern Lights Studio Group, after three years of development, brought Lili's Little Kingdom, a title set in a tiny kingdom on a desk (cross-platform interoperability)officially into its first test. In June, the official team announced that the game had reached 10 million pre-registrations across all platforms;

NetEase has two products: Starry Friends and Shanhai Journey.

The former stands out for its visual “Cube Star” design and its “multiplayer party game” gameplay. The PC early-access version officially launched on April 28. It has not yet officially launched on Steam, and the mobile version has not yet received an official release date, but the App Store pre-order page shows a June 28 launch;

The latter focuses on sky-island travel and superpower themes. Although it was first revealed as early as Gamescom 2024, there had been no new information afterward until NetEase teased major news for June at this year's 520 conference;

HoYoverse's Starry Sky Valley, positioned as a pastoral life simulation game and integrating the core experiences of Animal Crossing and Stardew Valley, recently completed its second beta test, the “Star Journey Test.”

The entry of major publishers corresponds to higher investment, more refined world-building, and more immersive narrative experiences. This will inevitably raise the already high entry barrier for life simulation.

Therefore, for such a high-investment, slow-validation, word-of-mouth-dependent category, even if major titles launch intensively in the future, only products that truly find differentiated expression and balance content, community, and monetization are likely to remain for the long term.