文

A

In May 2026, Vietnam’s economy continued its growth trajectory, with stronger domestic consumption coexisting with inflationary pressure.

According to data from Vietnam’s General Statistics Office (GSO), retail sales of goods and services revenue reached approximately VND 3,185 trillion in the first five months, up 11.2% YoY, with real growth of 6.1%, indicating continued recovery in household consumption. In May alone, YoY growth rose to 11.8%, while discretionary consumption categories such as accommodation and catering, tourism, and apparel all saw a strong rebound.

However, this growth does not appear to have translated into stronger purchasing power. In May, Vietnam’s CPI rose to 5.6% YoY, a new high since 2020, as rising living costs continued to erode residents’ real income. DianDian analysis suggests that the widening mismatch between income and costs has further tightened cash flow among low- and middle-income groups, leading to a simultaneous rise in borrowing demand and credit risk.

Against this backdrop, approval authority for Vietnam’s fintech regulatory sandbox has begun to be delegated to the local level, while consumer credit pilots are accelerating. In the short term, funding gaps and supportive policies together provide a floor for credit expansion, but asset-quality pressure is accumulating. The quality of future growth will still depend on whether inflation and funding costs can stabilize.

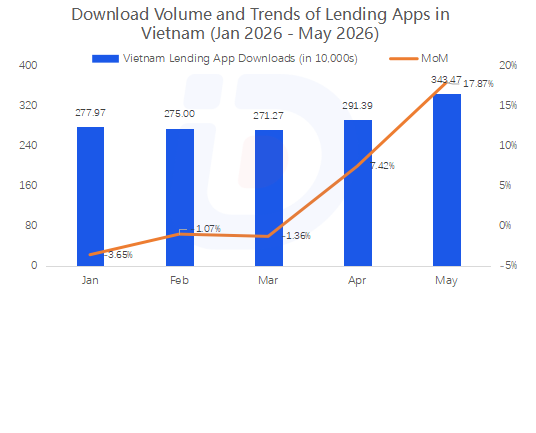

I. Industry Download Scale: Lending App Downloads Jumped to 3.4347 Million in May, Surging 17.87% MoM

From the perspective of lending app downloads, the demand-side breakout has already been clearly confirmed. In the first three months of 2026, Vietnam’s lending apps averaged around 2.75 million monthly downloads, with slight negative MoM growth continuing. A turning point appeared in April, when downloads rebounded to 2.9139 million and MoM growth turned positive at 7.42%; in May, downloads further jumped to 3.4347 million, surging 17.87% MoM and reaching a new high for the first five months.

II. Industry Landscape: FE ONLINE 2.0 Declines in Both Metrics, PT Vay Nhanh Active Users Grow Nearly 30%, while H Vaymuong/Tim TiềnContinues to Be Cleared Out

Against the backdrop of market expansion, industry concentration remained relatively high but has not yet entered a stage of absolute convergence.According to DianDian monitoring, the Top 20 apps recorded a combined download volume of around 1.9 million in May, accounting for 55% of the total market of 3.43 million, meaning long-tail apps still contributed nearly half of total traffic.

Monthly active users were also highly concentrated. The FE ecosystem (FE ONLINE 2.0 + the legacy FE Online version)ranked first with combined MAU of around 1.47 million; the Home Credit ecosystem (Home Credit Tài Chính Online + the legacy Home Credit version)continued slight growth, with combined MAU of around 1.10 million, ranking second; VayDễrecorded 275,000 MAU, still far smaller than the first two players. Together, the three accounted for around 54% of total MAU among the Top 20.

Among them, FE ONLINE 2.0 saw active users and downloads decline by 8.82% and 2.47% MoM, respectively. Although it still ranked first with around 1.006 million MAU, pressure on its existing user base was evident, and the scale gap with Home Credit narrowed. VayDễremained basically flat in active users (+0.94%), but downloads fell 8.78%, indicating weaker new-user acquisition momentum.

Among the Top 20, PT Vay Nhanh delivered the most outstanding performance. Since launching on the App Store on January 20, 2026, it has scaled quickly, maintaining more than 100,000 downloads for three consecutive months. This pushed its MAU in May to 155,000, up 29.64% MoM, allowing it to enter the local lending active-user ranking at No. 11 less than six months after launch.

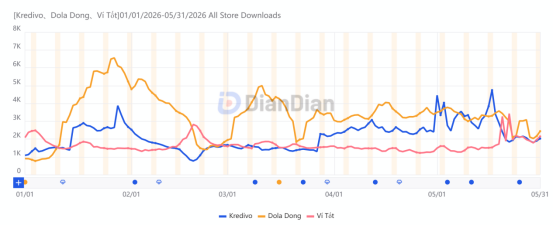

By contrast, Dola Dong showed a “strong first, then weak” trend from January to May 2026. After downloads reached a stage peak in January, they declined month by month, falling to 96,225 in May (-5.77% MoM), reflecting a gradual weakening of new-user acquisition momentum.

Kredivo, meanwhile, showed stronger recovery and rebound capabilities. Since its February downloadlow of 43,793, downloads have continued to recover, rising to 87,497 in May, up 15.74% MoM, indicating that growth momentum has partially recovered.

Ví Tốt recorded 54,833 downloads in May (+29.71% MoM), returning to the upper end of its nearly five-month range. From a longer-cycle perspective, its monthly downloads have fluctuated narrowly between 42,273 and 54,833, meaning it remains within its historical range overall without a trend-driven expansion or contraction.

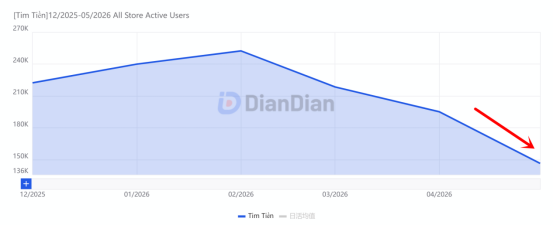

Among apps with notable declines in active users, particularly H Vaymuong was a typical case, with MAU down 24.88% MoM in May.The main reason may be that its corresponding Google Play app, Tim Tiền (the two share the same package name), was removed from Google Play on April 7, 2026, interrupting its core distribution channel and triggering a large-scale loss of existing users.

According to DianDian observations, the app developer PHU BAO ANH SERVICES AND TRADING COMPANY LIMITED claims to provide online loans of up to VND 50 million, but public business registration information shows that its main business only covers trade, services, and telecommunications.

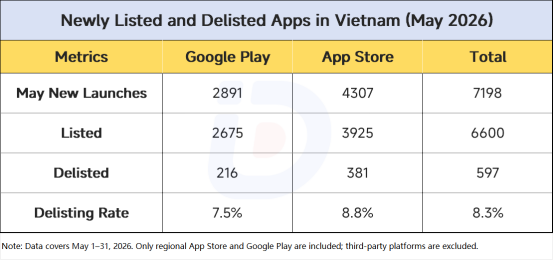

III. Regional Listings and Delistings: Tool Apps See a Delisting Rate of Around 10.6%, while Cross-Border Shell Apps Accelerate Localization Attempts

In terms of listings, Vietnam’s two major platforms continued to see high-frequency new app launches in May, with the App Store showing larger volume while Google Play remained more active.

DianDian monitoring shows that App Storenew listings in the month were approximately 1.49 timesthose on Google Play. However, delisting rates on both sides were around 8%, indicating that May was not a case of large-scale delisting after a short-term rush of new uploads, but rather a coexistence of continuous new listings and partial rapid clearing.

Lending-related apps accounted for less than 1% of total volume, and many were traffic-referral or pre-screening tools such as Check Eligibility and Credit Assistant. The delisting rate for such tools was around 10.6%, higher than the overall 8.3%, reflecting stricter platform review and control over lending-related apps.

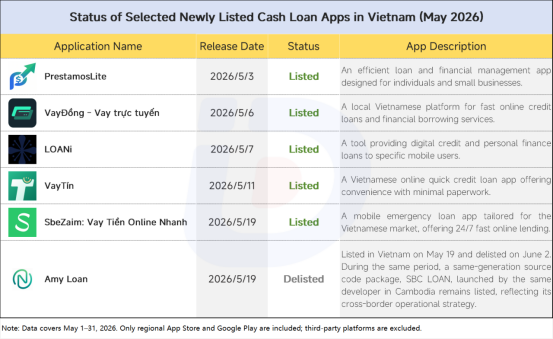

Status of Selected Newly Listed Cash Loan Apps in May:

[DianDian]Based on its global app store monitoring system, DianDian can track the full lifecycle of cash loan apps, including listings, delistings, and package changes, while identifying compliance red flags such as disguised shell apps and cross-store transfers, providing data support for cross-border fintech market analysis.

Industry Updates: Stricter Regulation of Large-Value Transfers, Regulatory Sandbox Approval Authority Delegated, and Leading Institutions Use Cashback to Drive Users Online

According to requirements from the State Bank of Vietnam (SBV), starting May 1, 2026, interbank transfers exceeding VND 500 million in a single transaction may no longer be automatically split by the system into multiple smaller instant transfers. Instead, they must be processed through the standard interbank clearing channel. At the same time, related large-value transactions will be included in key anti-money-laundering monitoring.

The implementation of the new rules is intended to close the loophole of evading supervision through “split transactions” and improve the transparency and traceability of large-value fund flows.It is expected that the impact on licensed institutions will be relatively limited, though they will need to further strengthen anti-money-laundering and fund monitoring capabilities. For illegal or gray-market lending businesses that rely on account nesting and transaction splitting, however, fund transfers will become more difficult and compliance risks will rise significantly.

https://vietnamnet.vn/en/banks-stop-processing-instant-24-7-transfers-for-transactions-about-vnd500mil-2511903.html

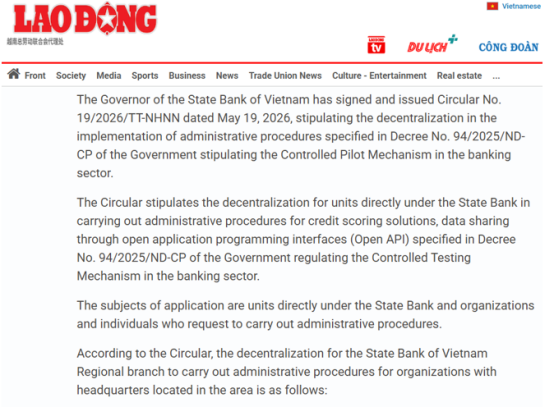

On May 19, 2026, the Governor of the State Bank of Vietnam signed and issued Circular No. 19/2026/TT-NHNN. The circular decentralizes administrative procedures for the previously implemented fintech pilot sandbox decree (Decree No. 94/2025/NĐ-CP).

The circular aims to implement the decree on a controlled trial mechanism in the banking sector (Decree No. 94/2025/ND-CP). Its core purpose is to delegate regulatory sandbox approval authority to SBV local branches and clarify the application, acceptance, and management processes for fintech innovations such as credit scoring and open APIs. This marks Vietnam’s fintech pilot program entering a localized and normalized approval stage, providing policy support for fintech companies to participate more quickly in compliant pilots.

https://news.laodong.vn/kinh-doanh/ngan-hang-nha-nuoc-chi-nhanh-khu-vuc-duoc-quyet-nhieu-thu-tuc-thu-nghiem-fintech-1709197.ldo?utm_source=chatgpt.com

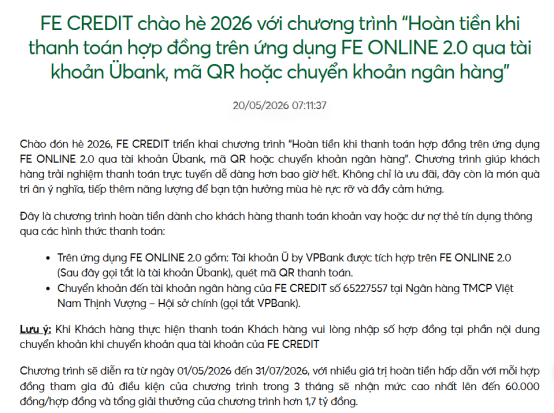

On May 20, 2026, FE CREDIT announced the launch of its “2026 Summer Cashback Program,” running from May 1 to July 31, encouraging users to repay loans or credit card bills through digital channels, including the Ü by VPBank account (Übank) inside the FE ONLINE 2.0 app, QR code scanning, and bank transfers. Eligible customers can receive cashback based on continuous usage, with a total prize pool exceeding VND 1.7 billion.

The campaign focuses on customers who previously used online repayment channels less frequently. Through staged cashback incentives, it guides users to migrate from traditional offline repayment methods to the company’s own app and digital payment channels. For FE CREDIT, this initiative can help increase user activity within the FE ONLINE ecosystem and improve online repayment penetration, further strengthening digital operations capabilities while reducing offline service and collection costs.

https://www.fecredit.com.vn/tin-tuc-khuyen-mai/khuyen-mai/fe-credit-chao-he-2026-voi-chuong-trinh-hoan-tien-khi-thanh-toan-hop-dong-tren-ung-dung-fe-online-20-qua-tai-khoan-uebank-ma-qr-hoac-chuyen-khoan-ngan-hang/

Overall, based on May’s market performance, Vietnam’s cash loan industry is in a phase where demand expansion and structural reshaping proceed in parallel, while growth momentum and compliance constraints are strengthening, showing three clear characteristics.

On the one hand, amid a macro environment of recovering consumption and inflationary pressure, residents’ short-term funding needs continued to be released, driving lending app downloads up 17.87% MoM and allowing the overall market to maintain its expansion trend. However, inflation is also eroding the debt repayment capacity of low- and middle-income groups, and signals of pressure on asset quality deserve attention.

On the other hand, divergence in the competitive landscape has intensified further. Leading platforms continue to maintain traffic and funding advantages, but the long-tail market still contributes nearly half of total traffic, meaning the industry has not yet fully converged. Emerging apps such as PT Vay Nhanh are rising quickly, while some previously high-growth platforms are slowing down or even exiting.

At the same time, anti-money-laundering regulation is strengthening, payment-system rules are tightening, and the fintech regulatory sandbox mechanism is accelerating implementation. Compliance constraints in Vietnam’s cash loan industry continue to rise. DianDian analysis believes that business models relying on gray-area operations and arbitrage space are being continuously compressed, and market positioning and clearing will continue to accelerate in parallel.