文

A

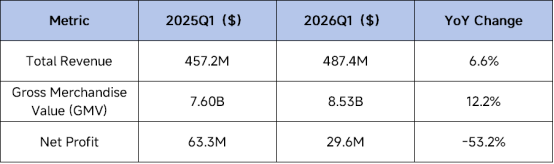

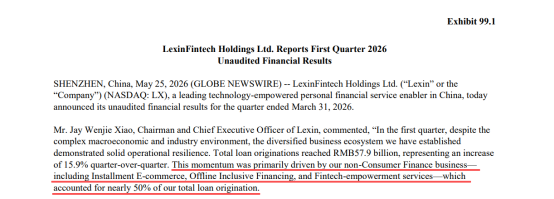

Recently, Lexin (NASDAQ: LX) released its unaudited financial results for the first quarter of 2026. During the reporting period, the company achieved total revenue of RMB 3.309 billion, up 6.6% YoY; loan facilitation volume reached RMB 57.898 billion, up 12.2% YoY and 15.9% QoQ. Overall business continued to grow against the headwinds despite pressure across the industry.

At the same time, however, net profit fell 53.2% YoY and outstanding loan balance declined 10.1% YoY, showing that the current situation is not as optimistic as it may appear. One trend worth noting is that Lexin’s growth sources are quietly changing: ecosystem businesses such as installment retail, offline inclusive finance, and B2B digital-intelligence technology now account for nearly 50% of transaction volume, while the revenue structure is accelerating its shift from a single credit-driven model toward diversified ecosystem collaboration. This suggests that Lexin is now in a critical window of transition from scale-driven growth to quality-driven growth.

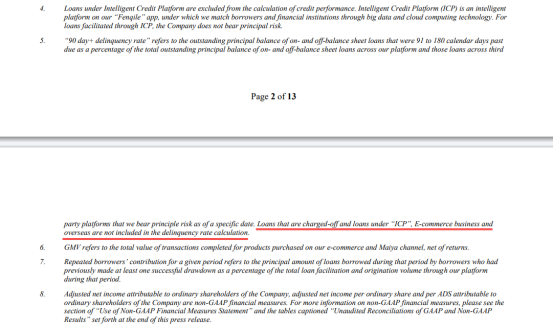

It is worth noting that Lexin stated in its delinquency-rate methodology that loans related to overseas business are not included in the calculation of the 90+ day delinquency rate. This means that overseas business, although not yet disclosed separately, has already shown some momentum and formally entered the company’s statistical scope, potentially becoming a new growth engine in the future.

Revenue Grew Against the Headwinds, While Profit Remained Under Pressure

Based on the core data from Lexin’s Q1 2026 financial report, its financial fundamentals showed a stage-specific pattern of recovery on the scale side and pressure absorption on the profit side. Total revenue in the first quarter reached RMB 3.309 billion, up 6.6% YoY and 8.7% QoQ, suggesting that revenue had returned to growth on the surface. However, net profit was RMB 201 million and Non-GAAP net profit was RMB 228 million, down 53.2% and 51.6% YoY respectively, indicating that the profit side remained under clear pressure.

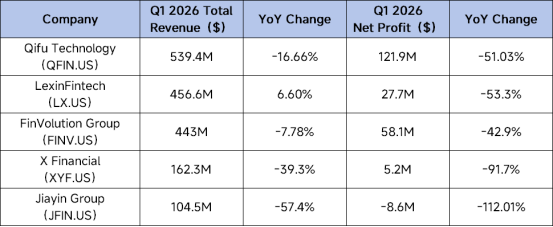

With the formal implementation last October of the Notice on Strengthening the Management of Commercial Banks’ Internet Loan-Assistance Business and Improving the Quality and Efficiency of Financial Services, tighter regulation led to an expected decline in the business of leading fintech companies. Compared horizontally with several leading fintech companies’ first-quarter results, Lexin’s Q1 performance was already above the passing line.

The reason for Lexin’s core Q1 financial pattern of “scale growth but profit decline” was not only the industry-wide shift toward more prudent operations under stronger regulation, but more directly the rise in risk costs and changes in business structure.

First are two indicators that reflect risk costs: Lexin’s 90+ day delinquency rate in the first quarter was 3.5%, up from 3.1% at the end of 2025; provisions for contingent guarantee liabilities reached RMB 959 million, higher than RMB 677 million in the same period last year. The increase in risk costs directly weighed on first-quarter profit performance.

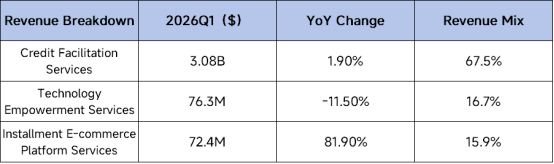

Second is the upfront cost brought by the growth of new businesses.According to the revenue composition data disclosed in the financial report, credit facilitation service revenue in the first quarter was RMB 2.232 billion, accounting for nearly 70% and remaining Lexin’s revenue base. Installment e-commerce platform service revenue reached RMB 525 million, up 81.9% YoY, making it the most visible structural highlight. This means installment e-commerce is no longer just a strategic concept, but has begun to make a real contribution to revenue.

Although installment e-commerce contributed the most eye-catching revenue growth this quarter, it differs from traditional credit-matching services by involving more links such as product transactions, fulfillment, channels, and user services. In the financial report, Lexin’s first-quarter sales cost, processing cost, and service cost all increased, showing that new business growth was accompanied by higher investment in operations and services. Therefore, at present, the installment e-commerce business is more like a new variable on the revenue side and has not yet fully translated into new support on the profit side.

Ecosystem Business TransformationBegan to Show Results

The most important change for Lexin this quarter was not in its traditional consumer-finance core business, but in the rising share of ecosystem businesses.This marks its gradual transition from a single online loan-assistance scenario platform toward a fintech ecosystem company with multi-scenario and multi-business-line collaboration.

According to the company’s management, in the first quarter of 2026, non-consumer-finance ecosystem businesses including installment e-commerce, offline inclusive finance, and B2B digital-intelligence technology already accounted for nearly 50% of total loan facilitation volume. This means Lexin’s new business lines are no longer merely strategic supplements, but are beginning to become core variables shaping the company’s growth structure.

Among them, the installment e-commerce business mentioned above stood out the most. In the first quarter, installment e-commerce GMV reached RMB 2.198 billion, up 95% YoY; users served by installment e-commerce exceeded 600,000. Compared with the low-single-digit growth of traditional credit facilitation services, installment e-commerce has become the clearest source of incremental growth in Lexin’s revenue structure, with its growth elasticity now validated. As a representative of Lexin’s ecosystem transformation, this business also preliminarily proves the necessity of this path.

Against the backdrop of tighter regulation, rising traffic costs, and asset-quality volatility, future competition will depend more on compliant operations, risk control, consumer-scenario accumulation, and technology-service capabilities. DianDian analysis believes that Lexin’s ecosystem-oriented attempt will bring higher investment and profit pressure in the short term; but in the medium to long term, if ecosystem businesses can continue to scale and gradually contribute profit, they will help Lexin gain an early advantage in the new competitive landscape for consumer-finance platforms.

Overseas Product Trends: Fintech Service Capabilities Are Being Validated

In overseas expansion, the single cash-loan model faces similar regulatory pressure, while the stronger fintech service capabilities built through ecosystem businesses can also provide Lexin with richer and more stable paths for going global.

Looking only at the financial report, Lexin’s disclosure on overseas business remains very limited. One relatively clear clue in the Q1 2026 report is that, in the methodology for the 90+ day delinquency rate, it states that, charged-off loans, as well as loans under ICP, e-commerce, and overseas businesses, are not included in the calculation of this delinquency rate.

Although the Q1 report did not separately disclose related data, this statement at least shows that overseas business has already entered Lexin’s internal business and risk-management scope. We may be able to glimpse part of the picture through the data performance of its overseas products.

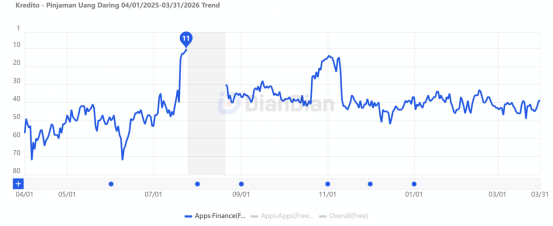

According to the overseas business information disclosed on Lexin’s official website, the company currently mainly operates two small-loan service apps: Kredito for users in Indonesia and Fortaprest for users in Mexico. DianDian supports one-click queries of target products’ downloads, revenue, and active-user performance across global markets, providing a higher-frequency and more forward-looking data window for observing overseas business.

Indonesia: A Compliance-Oriented Sample

Like the overseas expansion paths of most domestic fintech companies, Indonesia was also Lexin’s first stop. The online cash-loan platform Kredito was launched successively on Google Play and the App Store in Indonesia in Q3 2019, and obtained a financial lending institution license from Indonesia’s Financial Services Authority (OJK) in 2021, enabling it to conduct local business in compliance.

According to DianDian monitoring, Lexin’s core Indonesian product Kredito has performed relatively steadily on the free finance charts of the App Store and Google Play in Indonesia, with its ranking generally remaining within the top 50 over the past year and monthly downloads staying above 200,000. This indicates that it has a relatively stable local user base. Public information shows that Kredito already covers multiple borrowing scenarios including corporate employees, students, and small and micro business owners, fully reflecting Lexin’s localized operating capabilities in the Indonesian market.

According to Kredito’s official website, it has accumulated more than 1.12 million borrowers, over 120,000 active borrowers, and approximately IDR 7.3 trillion in cumulative loans issued. These figures are sufficient to validate Lexin’s compliance, localization, and long-term operating capabilities in Southeast Asia.

Mexico: A New Growth Window

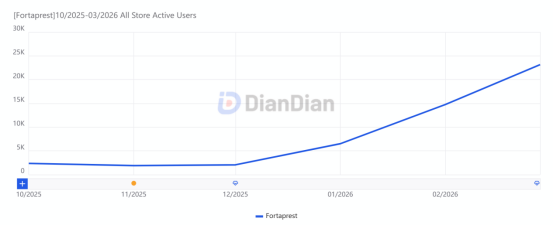

Fortaprest is a small-loan service product that Lexin launched successively on Google Play and the App Store in Mexico in 2023. Its App Store version was previously removed at the end of July 2024, and a new app was not relaunched until August last year. According to Lexin’s official information, Fortaprest, supported by the group’s accumulated capabilities in risk control, technology, and middle- and back-office systems, has already become one of Mexico’s leading financial service platforms. Compared with Kredito, Fortaprest better demonstrates Lexin’s customer acquisition and product-scaling capabilities in Latin America.

According to DianDian monitoring, the newly relaunched App Store version of Fortaprest in Mexico improved significantly in the first quarter of this year, with its ranking on Mexico’s free finance chart quickly climbing into the top 30. During the same period, the product’s downloads and active-user metrics both maintained steady growth; downloads across both platforms exceeded 620,000 in Q1. Its performance after relaunch also reflects that Lexin has already built a certain level of product awareness and traffic influence in Mexico’s cash-loan market.

DianDian analysis believes that Fortaprest’s value lies not merely in “adding another overseas app,” but in validating the feasibility of Lexin replicating its fintech products and service model in Latin America, while also providing an overseas validation scenario for its ecosystem transformation.

Conclusion

Overall, the signals released by Lexin’s Q1 financial report are not one-dimensional. On one hand, the company’s revenue and loan facilitation scale grew against the headwinds, and ecosystem businesses represented by installment e-commerce accounted for nearly half of the total, showing that Lexin is reducing its reliance on a single loan-assistance model. On the other hand, the YoY decline in net profit and the rise in risk costs also show that its current business transformation is still in a “proof process” stage marked by investment and pressure absorption.

What is more noteworthy is that Lexin is redeploying its accumulated fintech service capabilities and is redeploying them into new business scenarios for validation. Domestically, this validation is reflected in ecosystem businesses such as installment e-commerce, offline inclusive finance, and fintech empowerment; overseas, it is reflected in the continued operation and user growth of products such as Kredito and Fortaprest. As these new businesses move further from product data and user data toward financial data, whether Lexin can complete the leap from business switching to growth realization will be the top priority.

In the future, if overseas business can appear independently in the financial report, it may also mean that Lexin’s current round of business transformation has begun to enter a true harvest period.